Persefoni

SpydySense AI

AWARD

TIME has named Persefoni one of the World's Top GreenTech Companies of 2026.

Read more

Persefoni for Business

Overview

Carbon Footprint Measurement & Analytics

Sustainability Reporting

Regulatory Emissions Reporting

Stakeholder Emissions Reporting

Decarbonization Management

Scope 3 Supplier Engagement

Persefoni for Financial Services

Overview

Financed Emissions Accounting & Analytics

Investor Emissions Reporting

Decarbonization Management

Portfolio Company Engagement

Products

Persefoni for Business

Persefoni for Financial Services

Business

Overview

Carbon Footprint Measurement & Analytics

Sustainability Reporting

Regulatory Emissions Reporting

Stakeholder Emissions Reporting

Decarbonization Management

Scope 3 Supplier Engagement

Financial Services

Overview

Financed Emissions Accounting & Analytics

Investor Emissions Reporting

Decarbonization Management

Portfolio Company Engagement

PersefoniAI

California Compliance

SB 253

SB 261

Pricing

Customers

Pricing

Resources

Blog

Events & Webinars

Expert Content

Persefoni Academy

Sign Up Free

Sign In

Request Demo

Sign Up Free

Sign in

Translate

English (United States)

日本語 (日本)

English (United Kingdom)

German (Germany)

French (France)

Request Demo

Sign Up Free

Sign in

English (United States)

日本語 (日本)

English (United Kingdom)

German (Germany)

French (France)

Looking for our Logo?

Download our official logo from our Brand Assets page to represent and promote our brand with confidence.

Logos & Brand Assets

The Persefoni Blog

Search Blog Content

Insights

Company

Product

Newsletter

Insights

·

Wed

,

Jul

22

Carbon Offset Programs Guide and Examples for 2026

Insights

·

Tue

,

Jul

21

California SB 253 and SB 261: What Businesses Need to Know

Insights

·

Tue

,

Jun

30

Climate Policy Roundup - June 2026

Insights

·

Tue

,

Jun

23

The 10 Best Carbon Accounting Software in 2026

Company

·

Tue

,

Jun

09

Persefoni Named Among World's Top GreenTech Companies 2026 by TIME and Statista

Insights

·

Tue

,

Jun

02

Best Financed Emissions Software in 2026: Top 5 Platforms Compared

Product

·

Mon

,

May

18

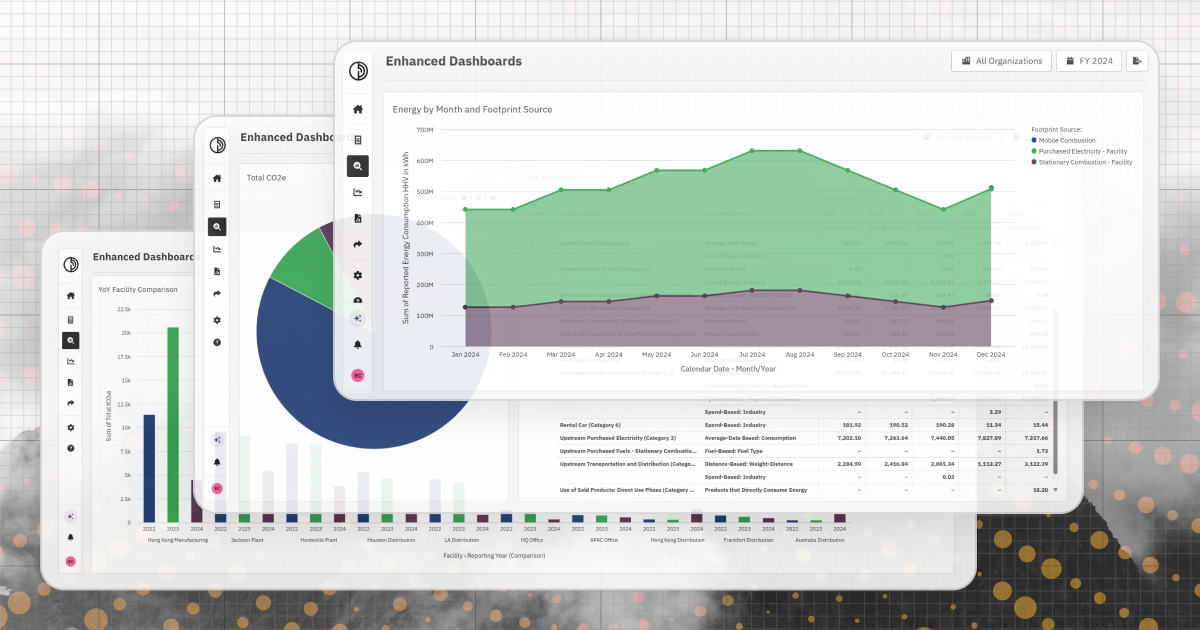

Unlock Granular Emissions Insights with Persefoni's Enhanced Dashboards

Insights

·

Tue

,

May

12

Understanding Bilan Carbone®: France’s Carbon Accounting Framework

Disclosures

·

Tue

,

May

12

KSDS: Korea’s ISSB-Aligned Sustainability Reporting Standards, Explained

Insights

·

Tue

,

May

12

Emissions Factors: What They Are and How to Use Them in Carbon Accounting

Insights

·

Thu

,

May

07

Canada’s Climate Risk Management and Disclosure Guidelines for Federally Regulated Financial Institutions

Insights

·

Thu

,

May

07

PCAF: Reporting Standard Beginner's Guide

Insights

·

Thu

,

May

07

What is SECR? Streamlined Energy and Carbon Reporting Explained

Product

·

Tue

,

May

05

Introducing Persefoni Analytics Agent: A New Way to Work With Your Sustainability Data

Company

·

Tue

,

Apr

07

Persefoni Selected by Amazon as a Featured Emissions Measurement and Reporting Solution on the Sustainability Exchange

Company

·

Wed

,

Mar

25

Persefoni Named Among America's Top GreenTech Companies 2026 by TIME and Statista for the Third Consecutive Year

Insights

·

Thu

,

Mar

19

Best CDP Reporting Software in 2026

Insights

·

Tue

,

Mar

10

A Step-by-Step Guide to Preparing Your First CDP Report

Insights

·

Tue

,

Mar

10

CDP Reporting: What It Is and Why It Matters

Insights

·

Tue

,

Mar

10

CDP: Carbon Disclosure Project Beginner’s Guide

Insights

·

Tue

,

Feb

24

Mexico’s ISSB-Aligned Sustainability Reporting Standards, Explained

Insights

·

Tue

,

Feb

24

Canadian Sustainability Standards (CSDS): An Explainer Guide

Insights

·

Fri

,

Jan

30

CSDDD - The EU’s Corporate Sustainability Due Diligence Directive, Explained

Insights

·

Fri

,

Jan

30

EU Carbon Border Adjustment Mechanism (CBAM): What to Expect

1 / 13

Close

Get the latest updates straight to your inbox

Sign up for our newsletter and stay ahead of the curve. With every edition, you'll receive the latest news, updates, and insights from our experts, straight to your inbox.

.png)

.png)

.png)